Stablecoin, Crypto, Blockchain

Original published in Vietnamese on July 4th, 2025 on the same blog pages.

The crypto industry today has drastically changed compared to four years ago, for better or worse. Many lessons learned over the years might no longer be applicable with the curveballs the cryptoverse is throwing at us.

Back in 2018, the total number of projects in the entire crypto market was fewer than 3,000. Fast forward to 2021, during the most recent biggest altcoin bull run, the amount of projects and tokens reached up to 30,000. With the help of AI tools and improvements in tokenizing toolboxes and frameworks, especially with the open-source culture, the total amount of tokens launching daily is between 5,000 and 10,000, totaling 37 million tokens in existence by 2025. That's a staggering number of tokens, impossible to keep track of, and hard to add value to. It takes a lot more to fill up tens of millions of "cups," which is why every project seems to find it difficult to gain traction. Anyone can launch a "worthless" meme-coin with a few clicks and a trendy name; on a good day, it can be life-changing. On a bad day, nothing happens, and no one would know or care. Years go by, and people would forget about it. This is what the crypto market has been filled with in the last few years, and it's also how most people, both inside and outside the industry, have viewed cryptocurrencies. Even large projects backed by Tier 1 Venture Capital funds (VCs) struggle to generate meaningful revenue or grow their user base, failing to achieve their promised product-market fit. When the vesting timeline arrives and the "cup is half-filled," the token price typically dumps for a few months before becoming a line in the history books. The industry feels rough, even as Bitcoin consistently hits new all-time highs (ATH), breaking through the $111k ceiling; Circle IPO'd and saw a 6x increase, and Coinbase reached new ATHs.

The Lagging Effects of Hostage Regulatory Environments

Looking back, the "hostage regulatory environment" created by SEC Chairman Gary Gensler and the most recent government administration has only created a restrictive sandbox for founders and builders. It's a "hostage room" where regulatory notices and lawsuits can arrive any day of the week, without clear guidance. So, what do smart people do? They get bored, create a few random, fun, and scammy projects, cash out, and many of them simply quit. Many others have learned to play "narrative games," which can also be profitable and successful in terms of financial gains, but at the cost of others losing money downstream – a true zero-sum game, with the side effect of millions of people losing trust in the industry and public blockchain solutions.

However, to be fair, even if you built useful products, most people wouldn't be able to use them anyway. Businesses wouldn't even be able to try them without legal scrutiny concerns. No matter how good your products are built, they quickly hit a revenue ceiling within a sandboxed community and struggle with both product and business growth, gaining almost no users if your products exclude gamblers and speculators. When there's no intrinsic value and no real revenue, the industry captures almost no market share of traditional financial infrastructure, and the value equation of the space becomes dominated by speculative factors. The usefulness of public blockchain technology in the last few years has touched nothing outside of "vibe," "meme," and "gambling" – so-called "prediction markets". Crypto tokens, or digital assets, have become nothing more or less than non-expiring lottery tickets that can give you a 100x return based on a cute animal logo or a news headline. Why would the technical differences of the network matter if there aren't enough enterprises and average users to push the platforms to their stress-testing limits? What would distinguish useful projects and platforms from useless tokens with a cute logo?

And that was the state of crypto before November 2024. But I believe it's changing, and the industry is turning a new page, at least for the next four years.

The Regulatory Headwind Finally Stopped

After the U.S. Election in November, not only are we getting a crypto-friendly U.S. president, but also the most pro-crypto Congress in history. Within a few weeks after January 20th, all restrictions against crypto projects were lifted, and all major investigations that had been ongoing for years were dropped. Guidance is being developed, and the U.S. has recognized Bitcoin and Digital Assets, placing them on Nations' Treasuries. The U.S. Congress is drafting a bill on a stablecoin framework, and the biggest payment companies in the world – PayPal and Stripe – are issuing their own stablecoins. Big investment institutions are racing each other to tokenize their assets onto public blockchains.

Stablecoin is the First Product-Market Fit Hitting Mass Scaling

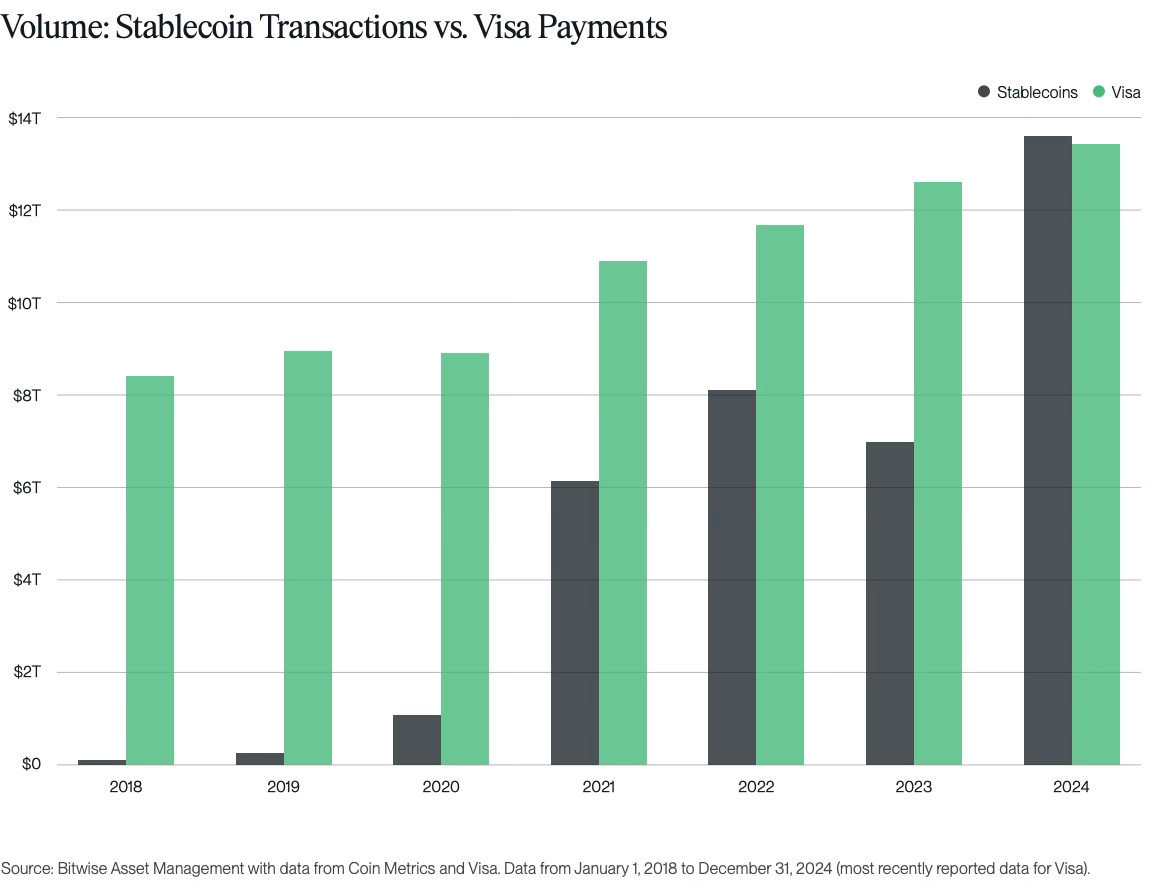

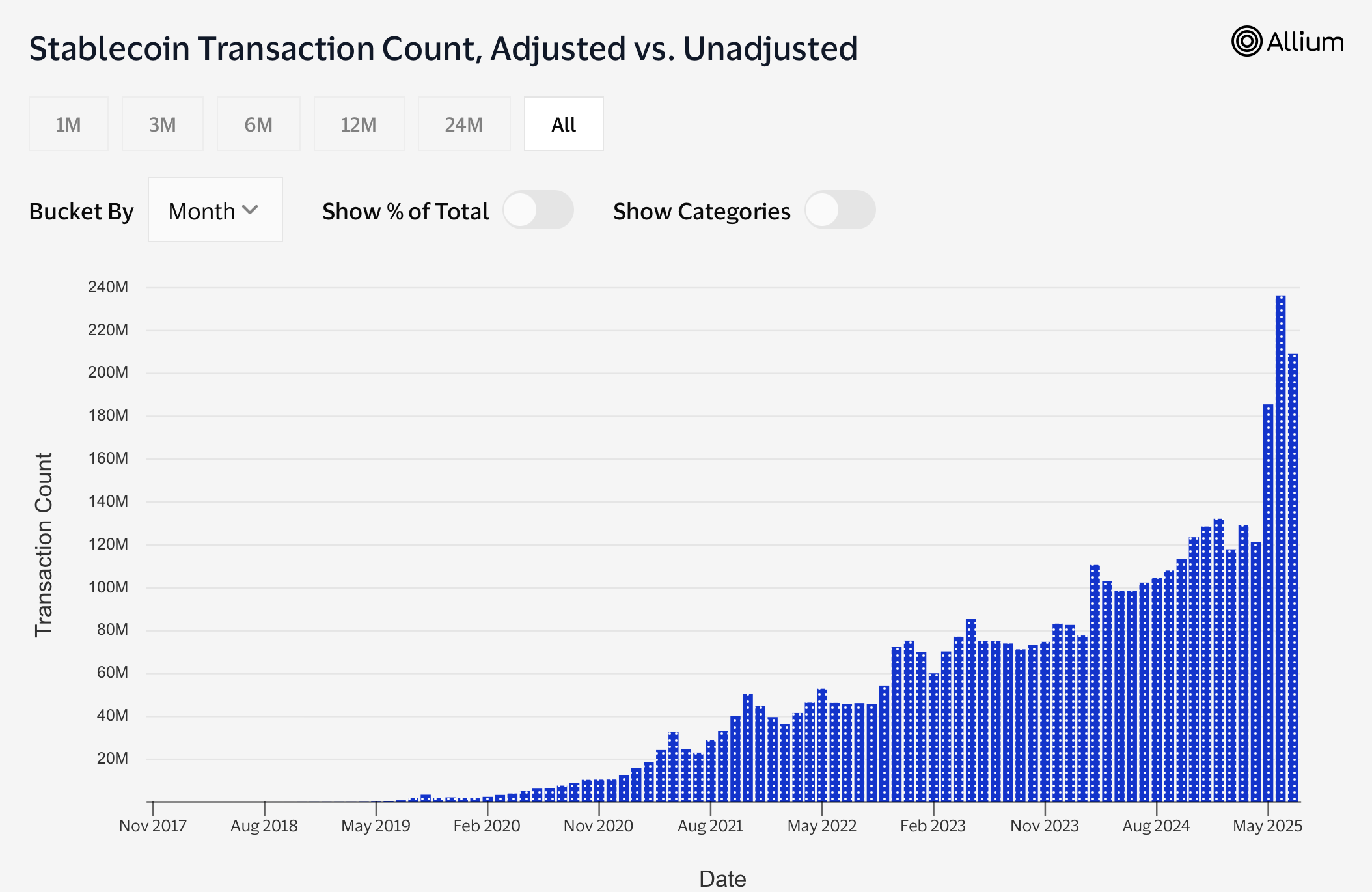

In 2024, stablecoins surpassed Visa in transaction volume for the first time ever. This proves that public blockchain "railroads" are reaching the masses, even amidst a hawkish legal environment, with their biggest product-market fit: stablecoins.

Stablecoins are digital crypto tokens that live natively on public blockchains and mimic the value of fiat currencies. The dominant stablecoins are issued by trusted parties like Circle and Tether, backed by a combination of real-world assets, allowing holders to redeem 1 USDC = 1 USDT = 1 USD at any point in time. Many different types of stablecoins have been market-tested over time, including asset-backed stablecoins (USDT, USDC) and algorithmic stablecoins like LUNA-UST, whose explosion and subsequent collapse with FTX definitely remain in history. These stablecoins, once issued on public blockchains (Ethereum, Solana, Base, etc.), can flow freely across them. Although most public blockchains are censorship-resistant, trusted parties issuing these stablecoins can flag fraudulent tokens. While they cannot stop these tokens from flowing between wallets on the networks, they can exercise some control over redemption when people want to off-ramp their money (converting stablecoins into USD in bank accounts).

You can think of the legacy banking system as a single payment ground where everyone has to register with banks to transact within the economy. That's the definition of "permissioned" – banks have to give you permission to use their payment networks. Differently, on public blockchains like Bitcoin, Ethereum, Solana, or Base, you don't have to ask anyone to open a wallet and start using these payment networks – that's "permissionless". The public blockchain, or "transaction settlement layers," is the public financial infrastructure. Stripe offered a brilliant analogy, comparing public blockchains to public roads, where anyone with internet access can create a wallet and "walk" on this payment ground. On this digital payment ground, anyone can create a business and transact without requiring bank accounts or intermediaries.

Each of these settlement layers has different technical approaches, given a different set of constraints and benefits. Decentralization is a measurement of a network's security assumption, as these are structured as decentralized networks where security authorities are spread out to many validation points to decrease the risk of network failure. Going back to the public road analogy, this means it's safer, with a lower risk of roads shutting down, and anyone can set up a business on that ground without censorship or asking anyone's permission, and no one can take your money away regardless of political beliefs. The beauty of seeing this as a public road is that people contribute to it as public goods and then use it as public goods. Although some will benefit more than others and in different ways (someone uses the park more, others own real estate close to the park).

Stablecoins are like ride-sharing services – products built and operating on top of these public payment "railroads". Instead of transferring value with native tokens (i.e., BTC, ETH, SOL), you can use stablecoins (USDC, USDT) as an efficient and familiar medium of exchange for transferring value on the public railroad. Moreover, as everyone in the world is familiar with the concept of fiat currencies, stablecoins are achieving mass adoption very quickly, showing no signs of stopping.

As of the time of writing, an important bill called the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act) is making its way to Trump's desk in the U.S. legal system. It's likely that the bill will reach the President's desk, and he will sign it given his very friendly attitude toward crypto.

Circle's IPO and Their Eye-Balling Success

Recently, Circle – the second-largest stablecoin issuer in the world and the only "free-range" operating business in the U.S. issuing USDC – went public on the U.S. stock market with a valuation of $6.8 billion, or $31 per share. A week later, Circle's valuation jumped to nearly $43 billion, with the price per share at $178 at the time of writing.

Stablecoin issuers are interesting businesses because they are essentially money market funds without the need to distribute interest to investors. One USDC is backed by $1 worth of T-Bills and fixed-income instruments. These fixed-income instruments pay out around 2-5% interest every year, and stablecoin issuers are not required to distribute any of this interest to stablecoin holders. However, Circle has been finding ways to give these yields back to stablecoin holders in various forms, such as Coinbase allowing users to receive 4.1% APY just by holding USDC in their account, without any staking. So, Circle's significant growth in market size and revenue is clear and has been priced into their market cap, but the pace of growth, distribution channels, changes in margin, and especially the impact of upcoming rate cuts are what the market is trying to figure out.

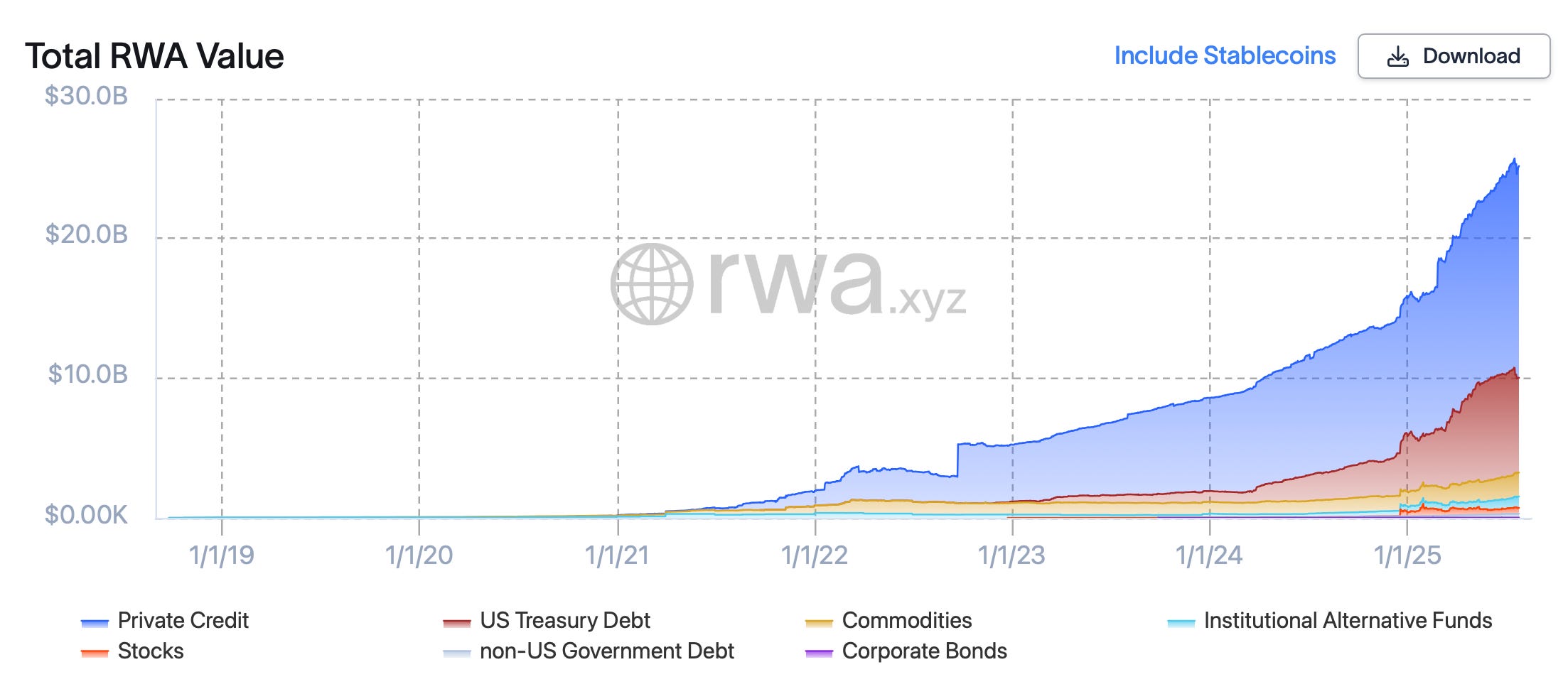

Tokenized Assets Growing at a Rapid Pace

On another front, Tokenized Assets (RWAs) have also been another rising star, generating buzz in institutional conversations. Excluding stablecoins, tokenized assets on-chain have quadrupled in two years and doubled compared to last year. Tokenized Private Credit and Tokenized US Treasury Products have accelerated the most, especially since Election Day. Including stablecoins, the total tokenized real-world assets brought onto these public financial "railroads" have been in discovery territory and show no sign of slowing down anytime soon.

Stripe, PayPal, Robinhood – all the "young, innovative players" in the payment "railroads" – clearly see crypto and blockchain as the future of the financial system. They are increasingly integrating with the tech stack and public infrastructure. Stripe acquired Bridge and Privy; PayPal has been issuing its own stablecoin for two years; and Robinhood, with millions of users, is launching its own Ethereum Layer 2 Blockchain leveraging Arbitrum SDK (Orbit). It's not that the public and institutions don't believe in blockchain; they just don't believe in weak fundamental altcoins or crypto as much.

Investing in the Public Financial Railroads - A Whole Different Story

These public ledgers are complex to understand. They are not as straightforward as Bitcoin – in fact, Bitcoin has nothing much to do with stablecoins. These different public financial "railroads" have different value propositions. Some are bigger and cheaper to transact; some are less public (permissioned-permissionless spectrum). Some are more decentralized or safer, meaning the probability of your wealth falling into a void if "the roads collapse" while you are transacting is statistically smaller.

The "road fees," when this infrastructure first gained attention during the 2020-2022 season, became very expensive. A transaction on Ethereum just to get a domain name during the hype season cost up to $200 in transaction fees. This led many others to try building digital grounds where the "road fee" is cheaper – such as Solana, Avalanche, Near, Polygon, BNB Chain, and dozens of other settlement layers. The goal was clear: to build payment settlement layers where the "road fees" are cheaper by accommodating some level of security assumptions – or decentralization – while providing elevated user experiences compared to a heavily congested Ethereum. Some claimed they figured out better technical approaches and gained popularity, attracting hundreds of billions of dollars in investment and accumulating trillions of dollars in market cap.

Having the right mental framework for the valuation of these networks is not easy. They are a combination of the ability to generate cash flow (gas fees), act as network collateral value (a feature of proof-of-stake), and are somewhat treated as a commodity (digital oil) where they are also used as gas fees for each transaction on the network. From the user and investor perspective, imagine this: you need oil to fill up your car to run around this digital ground, but this oil can also be used to generate more oil (staking). The price of this "digital oil" is also seen as the security collateral of the network. The more money parked on and the more transactions passing through these networks, the greater the economic incentive for bad actors to attack them. Hence, involved parties like stablecoin issuers and tokenized asset issuers will have an incentive to prop up the value of network market value, making it more costly to disrupt the networks.

From a usage perspective, institutions, applications, and users will need these native tokens to initiate any economic activities on this digital payment ground. It requires Ether to issue stablecoins, tokenize assets, transact, etc.. From the investor perspective, it's more like investing in public infrastructure and then collecting yield from the network's usage. For example, although it's true that all the base fees of each transaction on Ethereum are burnt, staked validators earn the Tips + MEV and the Consensus-Layer Reward (aka Default Block Reward) – estimated at 4% per year during quiet times and up to 8% during traffic surges. Solana, with the same proof-of-stake mechanism, yields somewhere between 8-11% (note that Solana's inflation rate is greater than Ethereum's). So yes, it is true that these are public infrastructures; they are open-sourced and permissionless, but everyone who wants to use or leverage them in their products and infrastructure will have to pay a gas fee to build and use these public ledgers.

A park during its first construction will be empty, but when it starts to become a fun place to hang out, people will invite each other to come, and that's when the network effect kicks in.

Ethereum Has Wildly Underperformed Regardless of Strong Fundamentals

In recent years, many Ethereum holders (including me) underestimated the impact of a hawkish regulatory environment on Ethereum relative to other networks. In this constrained sandbox, Ethereum's technical advantages and strong security assumptions have been underutilized, as usage demand hasn't been big enough to stress-test any public blockchain networks' security assumptions. One interesting insight recently picked up from Permissionless IV is that the old SEC was targeting Ethereum and marked it as a security, putting hidden pressure on those involved in The Merge. This insight had definitely been picked up by "the big guys" for years, and I can imagine the delta-neutral trade of longing BTC and shorting ETH has certainly been a successful trade on Wall Street.

Businesses and corporations, which often become customers of Ethereum for its decentralization and reliability, have been slow to roll out their products. The total of Layer 1s (L1s) and Layer 2s (L2s), totaling 2 million - 2.5 million transactions daily, still reflects a growing demand for public blockchains. The problem is that users are now paying a lot less for the "road fee" because the supply of blockspace simply outpaced its slow-growing demand, resulting in a big decline in staking yield for validators.

Note: Unlike Bitcoin, smart contract blockchain networks offer settlement with decentralized computation capability, which tends to be primarily bounded by computing limits, instead of block-size or the size of data it can contain within each producing block. The businesses and projects that are issuing, storing their wealth, and operating their financial services with assets on Ethereum will be the ones who care about Ethereum's network value, as it is a function of Proof of Stake (PoS). The higher the network value, the harder it is to attack the network. Meanwhile, the more valuable assets living on that chain get (RWAs, native assets, stablecoins), the higher the network value should be. This comparison will seem somewhat biased toward Ethereum, from the standpoint of value per byte and dollar volume the network is processing. However, Solana has been very robust and successful with its business development work, constantly finding ways to keep the chain relevant to the market even during tough times, and they fully deserve their outperformance over the last three years. In terms of user counts, Ethereum has not done so well, and I still doubt that it would change drastically in the next few years if we don't count in the L2s simply because the chain isn't designed to be capable of doing so. However, that doesn't mean the total gas revenue will not increase, as Ethereum will likely be used for higher-value transactions.

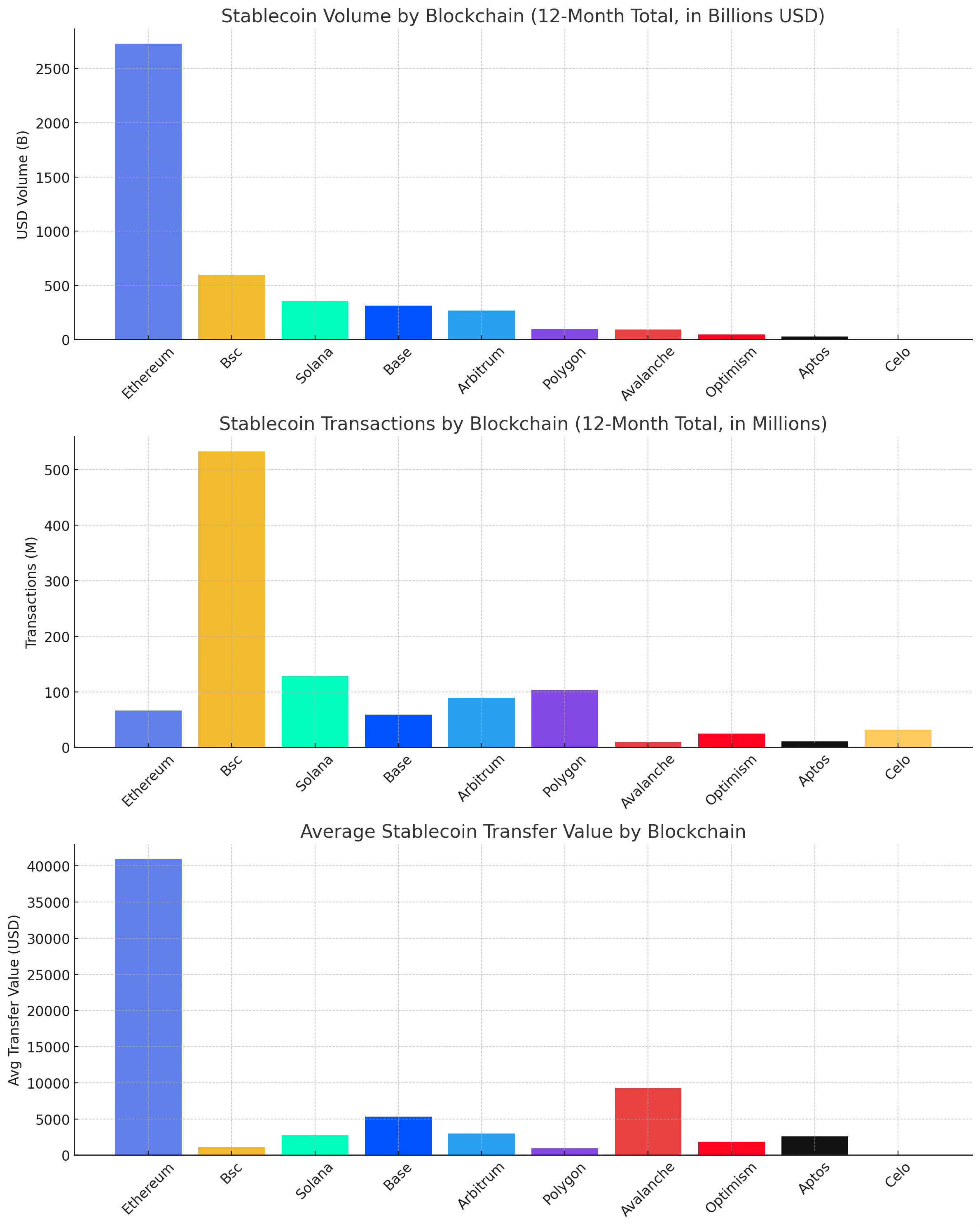

For example, in the last 12 months, Solana has facilitated almost double the amount of stablecoin transactions compared to Ethereum. However, Ethereum has totaled approximately eight times the amount of transaction volume in USD compared to Solana, resulting in $40,941 per transaction. That is far higher than the second place when it comes to the transfer value of each transaction. The average gas price of Ethereum has been below $1 (ranging between $0.2-$0.7 per transaction), while Solana and many other L2s offer 100 times cheaper transaction fees.

Stablecoins, at their core, will be recognized products. Users, most of the time, won't notice or care which chain they are using, but only about the transaction costs and the UI/UX. However, that thesis might hold true for the micropayment market. When it comes to the money market, where people hold, buy, invest, and store their wealth, people will start caring a bit more about the security assumptions of the network and whether the chain is safe. The surge in activities will start challenging the technical advantages of the networks again, and whichever can stand strong with the future stress-testing of the market when mass adoption floods in will prevail.

My definition of mass adoption still hasn't changed in years: that would be when we see a majority of transactions will not be used for speculation and trading purposes, but start shifting into more consumer spending transactions, lending and borrowing, capital flowing around the market between parties, etc.. My belief is that cheaper transaction fees will be favored for consumer spending applications, and more secure, stable, and reliable networks will be favored for financial infrastructure and wealth storage systems, and both will succeed on their own terms.

Everyone in the market has different beliefs, and that's something the financial market has taught me. No matter how many people around you and how strongly your elite circle believes in something, there's always someone else on the other side of your trades, betting against your opinions. And only time will tell which side of the table got it right. Even – with all due respect to the investing legend Warren Buffet – who the whole investing world praised three months ago because he was sitting on a pile of cash and the market heavily corrected (-20%) due to Trump's tariff. But then both the S&P 500 and the QQQ recovered and just hit their all-time high – leaving Berkshire Hathaway far underperforming the market (including the underperforming Apple stock he's still holding).

Disclaimer: I am somewhat speaking my book as an ETH and COIN holder, although the writing is for informational purposes and not financial advice. Please read it at your own risk.

Chí